China IOL Market Access — A Diagnostic

A 13-page document on how China’s intraocular lens reimbursement market actually works across its three regimes — now available on application.

Since our first note on the three reimbursement regimes governing China’s intraocular lens market, the most common question has been direct: what do the hospital economics actually look like inside each regime?

This document answers that question.

We have put together a 13-page diagnostic on how the market operates. It is structured to be useful to a strategy team in the first ten minutes and rigorous enough to defend to a finance function in the first hour.

What it contains

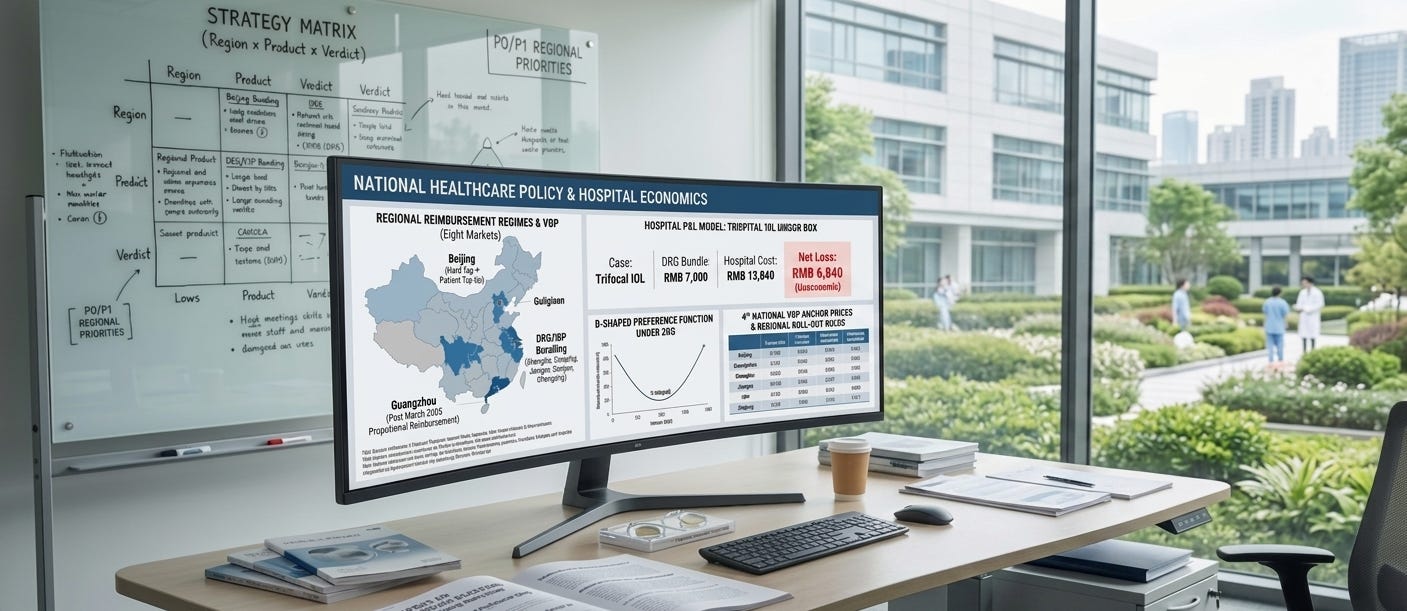

An executive summary of the three regimes and their commercial logics, Beijing’s hard cap with explicit patient top-up, Guangzhou’s post-March-2025 proportional reimbursement, and the DRG/DIP bundling now operating in Shanghai, Zhejiang, Jiangsu, Sichuan and Chongqing.

The provincial reimbursement map across eight markets with full source references.

The 4th national VBP anchor prices and the regional roll-out rules.

A hospital P&L model showing why the trifocal is uneconomic under DRG, a RMB 13,520 to RMB 6,680 hospital loss per case against a RMB 7,000 bundle.

The strategy matrix (region × product × verdict) and the P0/P1 regional priorities.

Two observations on physician behaviour that current market narratives miss: the U-shaped preference function under DRG, and dispute-aversion as a second, unnamed driver of IOL selection.

How to apply

The document is available on application, free of charge. We review each request individually before sending, this keeps the circulation traceable and the readership verified.

To apply, email intelligence@ophthallogix.com with the subject line “Diagnostic — application” and include five pieces of information: full name, work email (on a company domain), company name, job title, and LinkedIn profile URL. We use these to confirm we are sending the document to the right kind of reader. We aim to respond within three working days.

Substack subscription is open for readers who want to follow ongoing work on this and adjacent topics. Use the Subscribe button at the top or bottom of this post.

Key Implications

Companies managing intraocular lens portfolios across multiple Chinese provinces face three distinct commercial logics, not one. A strategy that treats China as a single market will misprice risk in at least one regime. The policy-execution gap is widest in DRG provinces, where the bundled payment structure makes premium IOLs structurally uneconomic for hospitals, a RMB 10,000-per-case loss that no amount of promotional effort will close without a policy carve-out. The immediate priority for any organisation with premium IOL exposure in China is to classify each target province by regime type before committing next quarter’s resources. This document provides the province-by-province framework for that classification.

— The OphthalLogix Intelligence Team

This content is for informational purposes only and does not constitute legal, regulatory, investment, or medical advice. China’s healthcare policy environment moves quickly; the status of any regulatory development should be verified independently before informing a commercial or compliance decision. OphthalLogix Intelligence accepts no liability for decisions made in reliance on this content.

intelligence@ophthallogix.com · www.ophthallogix.com