China’s IOL Procurement List Update: The RMB 9,090 Price Anchor and What Non-Selected Means Now

The National High-Value Medical Device Joint Procurement Office updated China’s intraocular lens procurement list on 16 April 2026.

I. What the List Actually Shows

The 20260416 version divides every IOL product into four categories. Selected products competed and won a price-based procurement slot; hospitals must purchase these to fulfil their annual agreement volumes. Viewed-as-selected products did not participate in the original competitive round but have since been added through a supplementary pathway, at a price no higher than the sponsoring company’s existing selected price. Non-selected products competed but did not win, or did not participate. Products outside the scope are explicitly excluded from this procurement exercise.

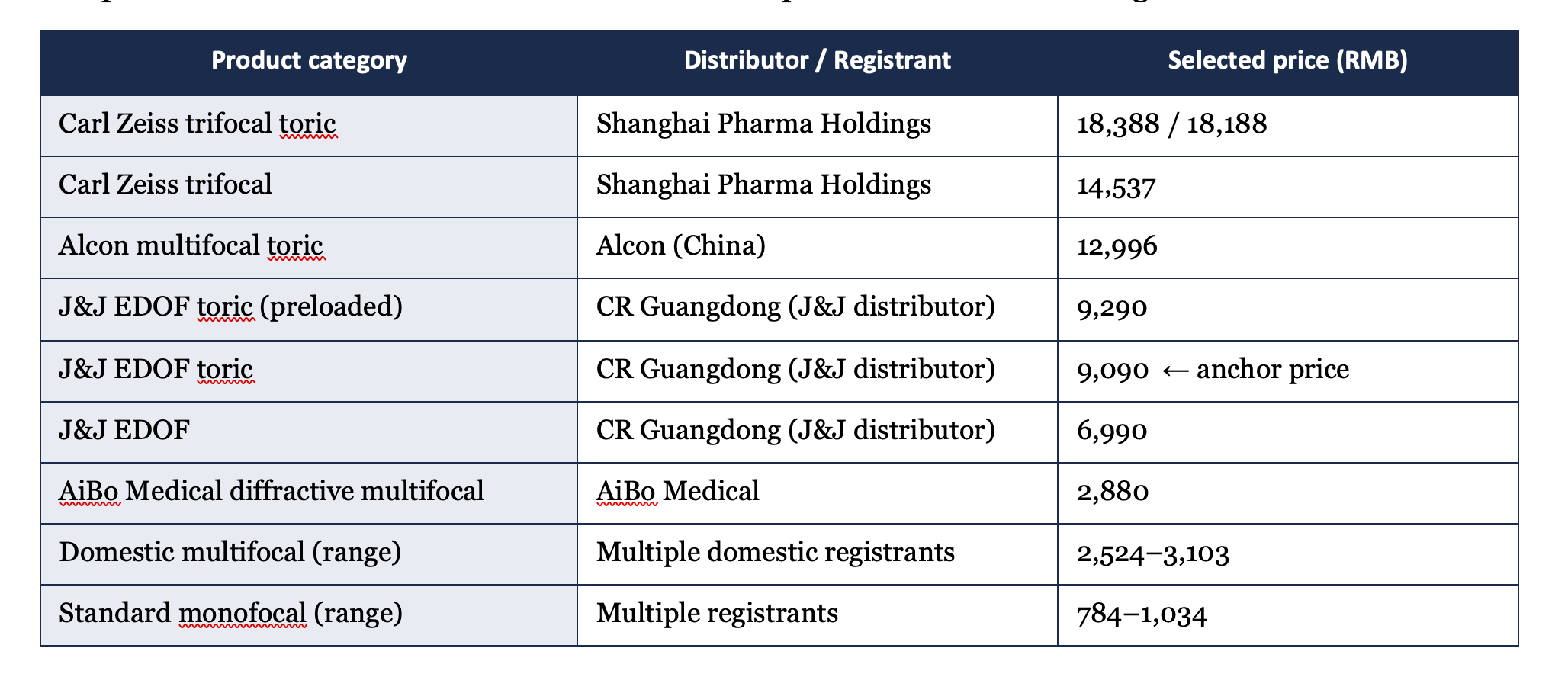

The premium end of the selected list establishes the price structure that now governs the market:

The non-selected section reveals how many products from major manufacturers currently sit outside the procurement framework. Multiple international and domestic companies have products in the non-selected category, including several with significant portfolios across monofocal and premium segments.

One detail worth noting precisely: Johnson & Johnson has products listed under two separate legal entities, its mainland distributor CR Guangdong (whose EDOF products are selected) and a separate direct entity. The procurement framework treats legal entity and product registration as the unit of analysis, not brand identity. Market access teams that model China exposure at the brand level rather than the entity and registration level will misread their own position.

II. The Public Hospital Market Is Already Decided

The 20260416 update is being published as procurement year two is in progress. Public hospitals in the procurement are required to fulfil at least 95 per cent of their prior year’s actual purchase volumes for selected products before any discretionary purchasing of non-selected products becomes operationally viable. Medical insurance departments actively monitor completion rates and follow up with institutions that fall behind.

The policy-execution gap here is not between what the policy says and what hospitals intend to do. It is between what market access teams assume about physician autonomy and what the system actually permits.

OphthalLogix assessment: Clinical practice within China’s public hospital ophthalmology system has adapted to the procurement list as the default selection framework. The list covers a clinically adequate range across monofocal, toric, multifocal, and EDOF categories, and the overwhelming majority of cataract surgery patients carry medical insurance of one type or another, which in practice fixes the choice to listed products. When non-selected products are discussed with clinicians, the response is typically not opposition but unfamiliarity. Non-selected products have not entered the clinical conversation.

The mechanism behind that unfamiliarity is structural, not personal. Hospital procurement departments configure HIS (hospital information systems) and SPD (supply and distribution) platforms to display only selected or viewed-as-selected products at the point of clinical decision-making. Non-selected products are not visible in the system at the moment a physician places an order. A physician choosing an IOL sees the options the system presents. Options that the system does not present do not exist in clinical practice.

This is passive exclusion, not active rejection. The distinction matters for how market access teams should interpret hospital-level data, and for where commercial effort is directed.

III. “Viewed as Selected” — Two Mechanisms, Two Different Realities

The supplementary pathway is frequently cited as the route through which non-selected premium IOLs maintain hospital access. The mechanism deserves close reading because it operates very differently depending on the status of the company using it.

Products from companies with existing selected status can be added at a price no higher than that company’s existing selected price for the equivalent category. These additions enter the full selected system: they count towards hospital annual procurement quotas, carry the standard medical insurance payment rate, and generate the same compliance credit as originally selected products.

Products from companies without selected status may be listed at a price no higher than the category average of selected products. However, they receive only one benefit: exemption from non-selected product classification in hospital performance assessments. They do not generate procurement quota credit. Hospitals must still fulfil their volume obligations through genuinely selected products before these products become operationally accessible.

OphthalLogix assessment: For companies with selected status, Johnson & Johnson added a new EDOF product to the list within approximately 70 days of regulatory approval. This is deliberate product management. The pathway allows J&J to extend its procurement footprint for each new product launch without re-entering competitive bidding, as long as the price remains within its existing selected band. For companies without selected status, the pathway offers hospital access without quota credit. It is a survival mechanism, not a growth instrument. The distinction is the difference between a strategic tool and a temporary lifeline.

Companies without selected status that are currently relying on the viewed-as-selected pathway should treat that position as time-limited. The third procurement year, beginning in mid-2026, will determine whether the pathway remains available as the overall framework matures.

IV. RMB 9,090 — What That Price Actually Represents

The 20260416 list shows Johnson & Johnson’s EDOF toric lens at RMB 9,090, and the preloaded version at RMB 9,290. These did not enter through competitive bidding. They entered through the supplementary pathway, at a price J&J chose to accept.

The question of whether 9,090 is a market-clearing price or a strategic price has a clear answer: it is a strategic price.

Alcon entered the fourth national procurement batch with pricing that brought trifocal and premium lens categories from above RMB 20,000 to below RMB 10,000. The overall average price reduction across the IOL category was approximately 60 per cent. J&J’s decision to enter the supplementary pathway at 9,090 was a response to that price floor, not an independent assessment of what the product is worth.

The logic is competitive foreclosure. By accepting 9,090 as the entry price for its EDOF toric, J&J secured procurement access and simultaneously set the reference price that any subsequent EDOF entrant will be measured against. Any competitor seeking to enter the supplementary pathway for an EDOF toric product must price at or below the average of existing selected prices in that category, a figure that is now anchored, in part, by J&J’s 9,090.

OphthalLogix assessment: In China’s premium IOL market, Johnson & Johnson holds a leading position in EDOF development, clinical training infrastructure, and real-world adoption. Its clinical credibility in this segment is ahead of other manufacturers. The 9,090 price point benefits from that credibility; it is not priced for parity with lesser-regarded products. At this level, J&J’s margin on the Chinese public hospital market is almost certainly under structural pressure. This product is priced to hold market access, not to generate the returns that its global pricing history would suggest are sustainable.

The commercial question is not whether 9,090 becomes the reference price. It already is. The question is whether your company’s products are on the right side of that reference when the third procurement year framework is confirmed in mid-2026. A company that delays this decision by two procurement years will find the reference price set, the quota volumes committed, and the clinical relationships in place for competitors.

V. Key Implications

For MNC market access teams: the 20260416 list is not static. The procurement office updates it periodically; this version follows several prior updates. Teams should verify current product registration status against the list, confirm which legal entity is submitting which products in which category, and audit whether any non-selected products relying on a viewed-as-selected position are still meeting the price conditions required. The entity-level split in the J&J data is a prompt to do this audit at the registration level, not the brand level.

For companies with selected status: the supplementary pathway is available now and should be used actively. Every product that gains selected or viewed-as-selected status before the third procurement year’s framework is confirmed strengthens the position. The window between regulatory approval and supplementary listing, approximately 70 days in J&J’s case, is a workable timeline if the process is prepared in advance.

For companies without selected status: the honest assessment is that the public hospital market for listed IOL categories is largely decided. The policy-execution gap runs entirely against non-selected products: the procurement quota must be filled first, the HIS system does not display non-selected options, and clinical teams have adapted their practice to the list. Commercial activity directed at public hospital formulary access for non-selected premium IOLs will generate diminishing returns. The more productive question is whether a pathway to selected or viewed-as-selected status is achievable before the third year closes.

For investors: the list structure is stable enough to model. The premium IOL segment has a confirmed price range from RMB 784 to RMB 18,388, with the high end representing Zeiss trifocal toric. The EDOF category has an established anchor at RMB 9,090. The policy-execution gap that matters for returns is not the gap between selected and non-selected — that is resolved. It is the gap between stated procurement price and actual margin, which at these price levels is not publicly disclosed by most participants and warrants independent verification.

This content is for informational purposes only and does not constitute legal, regulatory, investment, or medical advice. China’s healthcare policy environment moves quickly; the status of any regulatory development should be verified independently before informing a commercial or compliance decision. OphthalLogix Intelligence accepts no liability for decisions made in reliance on this content.

— The OphthalLogix Intelligence Team · www.ophthallogix.com · intelligence@ophthallogix.com